Most of the people think that credit and debt are both the same things and can be used interchangeably. But that is not true at all. Both credit and debt are different aspects and can’t be used at each other’s places. Credit and debt are indeed related to each other, but you can’t define them as the same thing when talking about their context.

Definition of Credit

There is no one way to explain credit; you will find a lot of definitions of credit. Credit could be the amount of money available for you that you can borrow or be allowed to borrow that amount of money. You get credits from the creditors based on your current credit score.

Only if you have a high credit score, you will get the desired amount of credit from the creditors with low-interest rates. If you have a low score of credit, they will not let you avail of the credit, or if they do, they will give you little credit, and the interest rate would be higher on that to be safe. Credit is used when you want to purchase something, and you are short on cash. It is the credit cards you use, which can be used under the definition of credit.

Definition of debt

Debt is the amount pending of the result of your credit. They are interlinked this way. You can have a debt only when you have taken out the credit amount. Debt is the amount that you borrowed, and you need to pay back to the person you borrowed it from. The debt amount needs to be paid with the incurred interest according to its rate. Some other fees are to be paid with the interest amount like monthly fee, initiation fee, or administration fee.

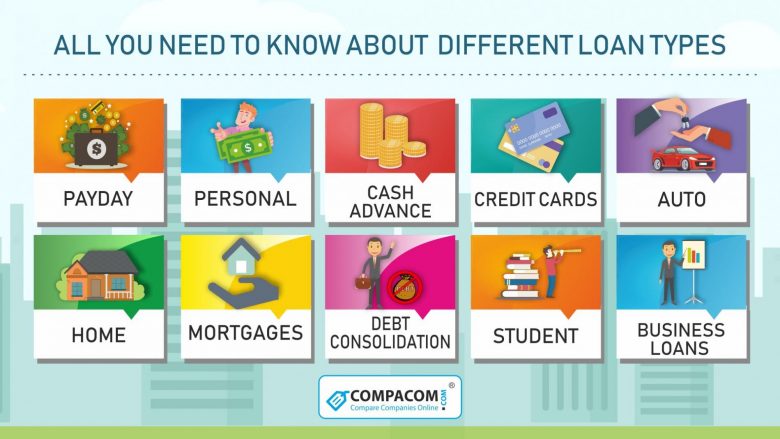

This can be explained in another way, like; if you have a car loan, house loan, or any other loan. It would be best if you played them back to the person who provided you the credit. For paying off these loans, people often have overdrafts or credit cards, which can provide them the credit they need to pay the loans on the terms and conditions which were agreed at the time of the loan. If you are having a hard time selling your house, https://www.fivehillsinvestors.com/ is always here to give you the assistance you need.

Is it good for you to take advantage of the high credits?

When you are good at paying back the amounts on time, the credit providers increase your credit amounts of credit cards, store cards, or overdrafts. This is an exciting thing, but it is up to you if you can take higher credit and then pay it back on time. Till now, you had the specific amount, but now that it has increased, you need increased income also for paying it back.

Having high credit can boost your credit score, but making the good use of the credit you are being provided falls at your hands and only on your shoulders if you end up being in a lot of debts.